Machine Learning in Fintech: How It Works, Use Cases & Real Examples

From ML Pilot to Production in Fintech

A practical guide to planning, execution, and compliant deployment

Fintech has moved beyond simple automation. In 2026, machine learning sits at the core of how financial products are built and scaled. The shift from rigid, rule-based systems to adaptive models means decisions are no longer based on static thresholds but on continuously evolving patterns across massive volumes of transaction and behavioral data.

At the same time, growing digital adoption and real-time user expectations have made this transition unavoidable. Customers expect instant approvals, personalized financial experiences, and fraud protection, all of which rely on machine learning systems working in the background. What was once a competitive advantage has now become a baseline requirement.

Regulatory pressure is also accelerating this shift. Guidelines influenced by institutions like the Reserve Bank of India and the European Commission are pushing fintech companies toward transparency, fairness, and explainability in AI-driven decisions. As a result, machine learning is no longer just about accuracy; it must also be compliant, auditable, and production-ready at scale.

How Fintech and Machine Learning Work Together

When financial technology companies began digitising banking services two decades ago, they created something invaluable: a continuous, high-resolution record of how millions of people and businesses handle money.

Every swipe, transfer, loan application, and market order generates data. Machine learning is the engine purpose-built to extract value from exactly this kind of dataset. This alignment exists because financial systems demand fast, data-driven decisions across areas like fraud detection, credit assessment, and trading. Unlike static rule-based systems, machine learning continuously adapts to new data and improves accuracy over time.

This shift is reflected in market adoption, with AI in fintech projected to grow rapidly over the next decade.

ML vs. Traditional Analytics: Why the Difference Matters

Traditional rule-based systems and static analytics served finance well for decades. But they have hard limits. A rule that says 'flag transactions over $10,000' misses sophisticated fraud. A FICO score that ignores rent payments excludes millions of creditworthy borrowers. ML breaks through these limits:

The shift in 2026 is even more pronounced. Financial institutions are moving beyond isolated ML use cases toward fully integrated, intelligent systems, including early forms of agentic automation where models not only predict but also trigger actions.

Regulatory developments, such as evolving EU AI governance frameworks and open banking expansions (such as PSD3), are further accelerating this transition by increasing data accessibility while enforcing stricter accountability.

In this environment, machine learning is not just a technological upgrade; it is the foundation for building competitive, compliant, and future-ready fintech systems.

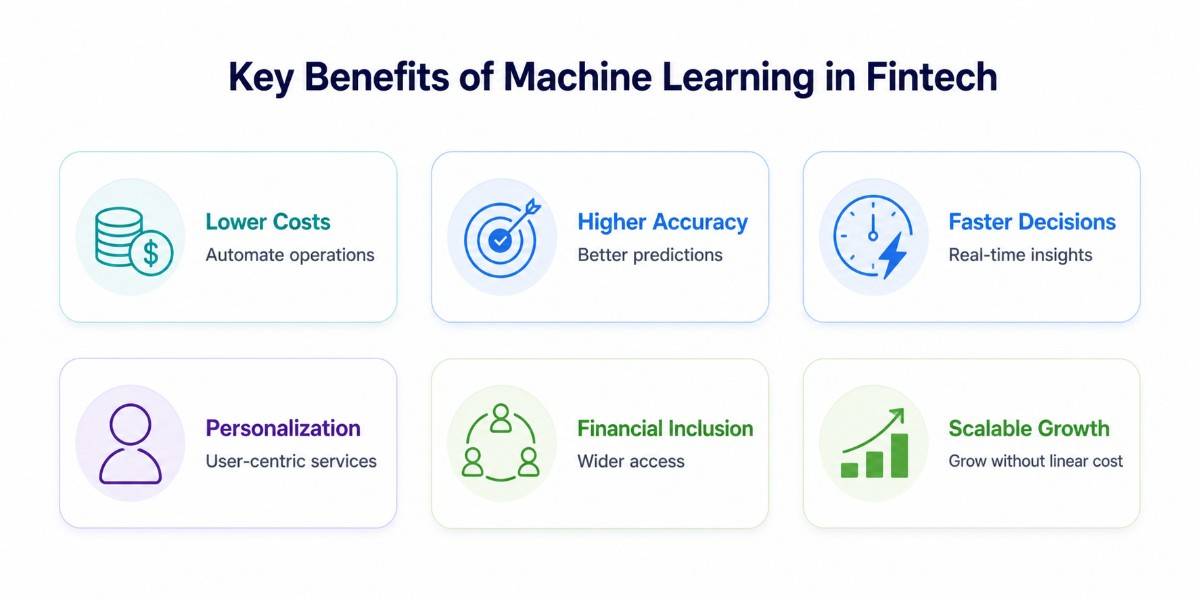

Key Benefits of Machine Learning in Fintech

The business case for ML in fintech is no longer theoretical. Here are the five categories of measurable benefit backed by 2026 data.

1. Lower Operational Costs

AI is on track to save the global financial industry $500 billion annually by 2030, with $120 billion already saved in 2025. Automation of document verification, loan processing, compliance monitoring, and transaction reconciliation removes labour-intensive manual steps.

For a mid-sized bank, ML-driven process automation typically reduces operational cost per transaction by 30–50% within 18 months of deployment.

2. Higher Decision Accuracy

ML models continuously learn from new data, which means their accuracy improves over time rather than degrading. In fraud detection, ML systems reduce false positives by 40–60% compared to rule-based predecessors, which translates directly into fewer legitimate customers having transactions blocked.

In credit scoring, ML models predict default risk 15–25% more accurately than traditional FICO-only approaches, enabling more precise pricing and lower loss rates.

3. Faster Decision Making

In financial services, latency is not just a technical metric; it is a business outcome. ML-powered fraud scoring operates in under 100 milliseconds, enabling real-time transaction decisions without adding friction to the customer experience.

Loan underwriting ML models reduce decision timelines from days to minutes. Algorithmic trading systems respond to market signals in microseconds. The competitive disadvantage of slow decisions is existential in 2026.

4. Personalized Customer Experience

ML allows financial institutions to treat each customer as an individual rather than a demographic segment. Spending pattern analysis, predictive saving nudges, personalised insurance pricing, and context-appropriate product recommendations are all delivered through ML pipelines that adapt to each individual's behaviour. Personalisation consistently drives measurable improvements in product adoption rates and customer retention.

5. Financial Inclusion

ML's ability to evaluate alternative data sources has a social dimension: it extends credit, insurance, and investment services to populations that legacy systems excluded. Thin-file borrowers, recent graduates, gig workers, and immigrants can now access credit based on demonstrated financial behaviour rather than the absence of a traditional credit history.

The Harvard Business Review has noted that when built correctly, ML models can actually reduce racial and gender bias in lending compared to human underwriters subject to unconscious bias.

6. Growth Without Linear Cost Increase

Traditional financial operations scale linearly, higher transaction volumes require more staff for compliance, underwriting, and support. This directly increases operating costs as the business grows.

Machine learning breaks this pattern by automating high-volume decisions such as fraud checks, credit evaluation, and transaction monitoring.

Once deployed, these systems can handle significantly higher volumes with only incremental infrastructure cost, allowing fintech platforms to grow faster without matching increases in operational expense.

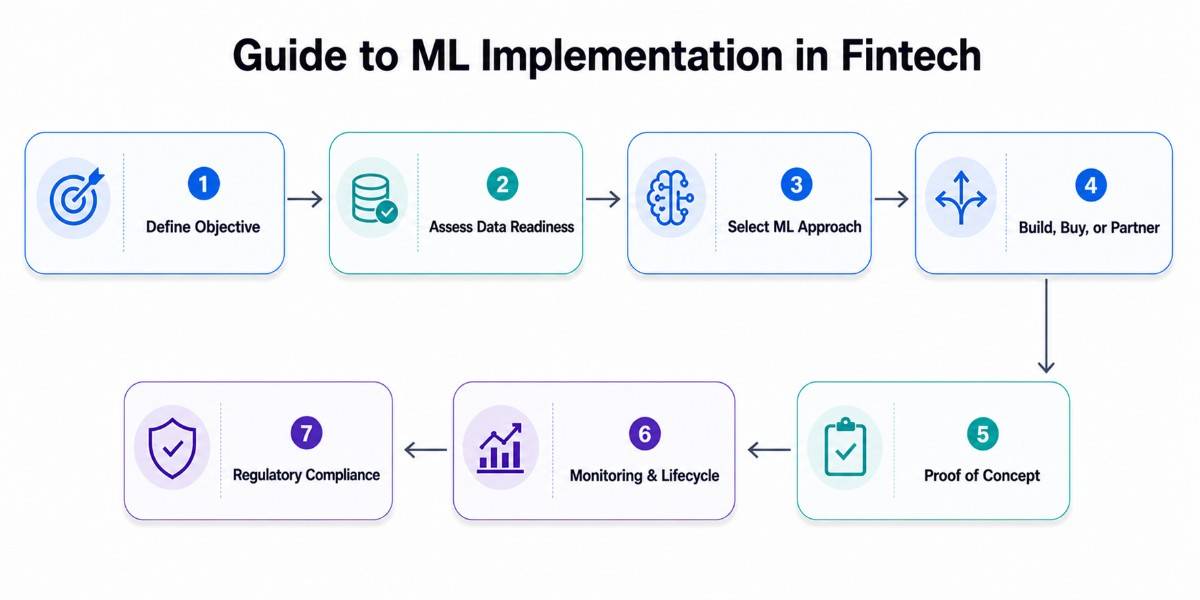

A Practical Guide to ML Implementation in Fintech

For teams exploring machine learning for fintech, the objective is not just to adopt the technology but to build systems that deliver measurable business outcomes. A structured approach ensures alignment between business goals, data readiness, model selection, and compliance requirements.

Step 1: Define the Business Objective

Machine learning initiatives should begin with a clearly defined and measurable objective. Instead of a broad goal such as adopting machine learning, focus on specific outcomes like reducing fraud losses, improving loan approval accuracy, or minimizing customer churn.

The solution must be directly linked to a key performance indicator. For example, a fraud detection system should aim to reduce false positives while maintaining strong detection rates. A clear problem definition ensures that the implementation remains focused and outcome-driven.

Step 2: Assess Data Readiness

The success of any machine learning system depends on the quality and availability of data. Financial institutions must evaluate the type of data they have, including transaction history, behavioral signals, and credit data, along with their consistency and completeness.

Labeling is another important factor. Supervised models require clearly labeled datasets, which often require significant effort to prepare. Strong data governance, validation processes, and structured pipelines are essential to ensure reliable model performance.

Step 3: Select the Appropriate ML Approach

Different use cases require different modeling approaches. Supervised learning is effective for classification problems such as fraud detection and credit scoring. Unsupervised learning helps identify anomalies in situations where patterns are not predefined.

Reinforcement learning is suitable for decision-making environments such as trading strategies. Choosing the correct approach requires a combination of technical expertise and domain understanding, including familiarity with the frameworks and libraries involved, to ensure that the model aligns with the intended business outcome.

Step 4: Choose Between Building, Buying, or Partnering

Organizations must decide how to implement machine learning capabilities. Building an in-house solution offers full control but requires significant investment in skilled talent and infrastructure. Purchasing software solutions can accelerate deployment but may limit flexibility and customization.

Partnering with a specialized development firm such as Code B provides a balanced approach. It enables faster implementation while ensuring that the solution is tailored to specific business needs.

Step 5: Begin with a Proof of Concept

A proof of concept allows organizations to validate feasibility before committing to a full-scale rollout. Starting with a focused use case, such as fraud detection on a limited dataset, helps evaluate performance and potential return on investment. This approach reduces risk and provides insights that guide further development and scaling.

Step 6: Monitoring and Lifecycle Management

Machine learning systems require continuous monitoring to maintain performance. Changes in user behavior or transaction patterns can affect model accuracy over time.

Establishing monitoring frameworks, retraining schedules, and performance tracking ensures that models remain effective.

This is essentially the operational side of LLMOps and model lifecycle management as it applies to production fintech systems. This transforms machine learning into an ongoing capability rather than a one-time implementation.

Step 7: Ensure Regulatory Compliance

Financial systems must comply with strict regulatory standards related to transparency, fairness, and accountability. This includes maintaining proper documentation, enabling model explainability, and conducting regular audits.

For credit, insurance, and AML applications, this means explainability documentation, bias testing across demographic groups, validation methodology documentation, and approval from your model risk management function.

Integrating compliance into the system from the beginning helps avoid future risks and ensures long-term sustainability.

From Strategy to Execution

Implementing machine learning in fintech requires more than selecting models. It involves aligning business objectives, data infrastructure, technical execution, and regulatory requirements into a cohesive system. Organizations that follow a structured approach are better positioned to deliver measurable value and scale effectively.

Core ML Models Used in Fintech Systems

For teams exploring “ML in fintech,” the real challenge isn’t understanding machine learning; it’s choosing the right models for specific financial problems and deploying them effectively.

Different models excel at different tasks: some are optimized for structured tabular data, others for sequences, text, or decision-making environments. In fintech, this choice directly impacts fraud detection accuracy, credit decisions, latency, and regulatory compliance.

Below is a practical breakdown of the most important machine learning models used in fintech systems today, what they do, how they work in real environments, and where they deliver the most value.

Logistic Regression

Logistic Regression remains one of the most widely used models in fintech, especially in credit scoring and loan approval systems. It works by estimating the probability of a binary outcome, such as whether a borrower will default or repay, based on input features like income, transaction history, and credit behavior.

Despite being a relatively simple model, it is highly effective when the relationships in the data are linear or near-linear. Its biggest advantage is interpretability, which makes it ideal for regulated environments.

Financial institutions can clearly explain why a decision was made, something that aligns well with compliance requirements influenced by bodies like the Reserve Bank of India.

In practice, Logistic Regression is often used as a baseline model or as part of a hybrid system, providing a transparent benchmark against more complex models.

Random Forest

Random Forest is an ensemble model that combines multiple decision trees to improve prediction accuracy and reduce overfitting.

In fintech, it is widely used for credit risk assessment and customer segmentation, where relationships between variables are complex and non-linear. It works by training multiple trees on different subsets of data and aggregating their outputs.

The strength of Random Forest lies in its ability to handle noisy and high-dimensional data without requiring extensive preprocessing. It can capture intricate feature interactions that simpler models miss.

This makes it particularly useful in scenarios like evaluating borrower profiles or detecting anomalies in transaction patterns, where multiple variables influence outcomes simultaneously.

XGBoost

XGBoost has become a dominant model in fintech due to its exceptional performance on structured financial data. It uses gradient boosting to iteratively improve predictions, making it highly accurate for tasks like fraud detection and real-time transaction scoring.

Many large-scale fintech systems rely on XGBoost because it balances speed and accuracy effectively. One of its key advantages is its ability to handle imbalanced datasets, which are common in fraud detection (where fraudulent transactions are rare).

It also supports regularization, helping prevent overfitting. In production systems, XGBoost is often deployed in real-time pipelines to score transactions within milliseconds, enabling immediate fraud prevention actions.

LSTM / RNN

Long Short-Term Memory (LSTM) networks and Recurrent Neural Networks (RNNs) are designed to process sequential data, making them ideal for financial time-series analysis. These models capture temporal dependencies, understanding how past events influence future outcomes.

In fintech, they are used for stock price prediction, transaction sequence analysis, and behavioral modeling. Their primary advantage is the ability to retain context over time, which is critical when analyzing patterns like spending behavior or market trends.

For example, an LSTM model can detect subtle changes in a user’s transaction sequence that may indicate fraud. However, they are more computationally intensive and require careful tuning, which makes them better suited for high-value use cases where temporal patterns are essential.

CNN

Convolutional Neural Networks (CNNs) are commonly associated with image processing, but in fintech, they play a key role in document analysis and OCR (optical character recognition).

These models are used in KYC processes to extract information from identity documents, bank statements, and financial forms.

CNNs excel at detecting visual patterns and features, enabling automated verification workflows. This reduces manual processing time and improves accuracy in onboarding systems.

For fintech companies handling large volumes of customer documents, CNN-based systems significantly enhance operational efficiency while maintaining compliance standards.

Transformer / BERT

Transformer-based models like BERT have transformed how fintech systems handle text and language data. These models understand context, making them highly effective for chatbots, customer support automation, sentiment analysis, and compliance monitoring.

In practice, they are used to analyze customer queries, detect intent, and even monitor financial communications for regulatory compliance. Their advantage lies in contextual understanding, which allows them to outperform traditional NLP models.

For example, they can interpret nuanced financial language in customer interactions or news sentiment that may impact trading strategies.

Reinforcement Learning

Reinforcement Learning (RL) is used in fintech for decision-making in dynamic environments, particularly in algorithmic trading and portfolio optimization. Unlike traditional models, RL learns by interacting with an environment and optimizing actions based on rewards.

This makes it highly effective for adaptive trading strategies, where market conditions change rapidly. RL models continuously refine their strategies based on outcomes, enabling more sophisticated and autonomous financial systems.

However, they require large amounts of data and careful design, making them more complex to implement compared to supervised learning models.

GAN

Generative Adversarial Networks (GANs) are used in fintech to generate synthetic data, which is especially valuable in scenarios where real data is limited or sensitive. For example, fraud cases are rare, making it difficult to train models. GANs can simulate realistic fraudulent transactions to improve model training.

Their key advantage is enabling data augmentation without compromising privacy. This is particularly important in regulated environments where sharing real financial data is restricted. One reason why AI in insurance, another heavily regulated vertical, faces the same synthetic data challenges as banking.

GANs help improve model strength while supporting compliance requirements around data protection.

Ensemble Methods & Explainability (SHAP in Fintech)

In modern fintech systems, single models are rarely used in isolation. Ensemble methods, such as combining XGBoost with LightGBM, are now standard for achieving higher accuracy and stability. These approaches reduce model bias and variance, making them more reliable in high-risk applications like fraud detection and credit scoring.

At the same time, explainability has become critical. Techniques like SHAP (SHapley Additive exPlanations) help interpret model predictions by showing how each feature contributes to a decision.

This is essential for regulatory compliance and aligns with expectations shaped by organizations like the European Commission, where transparency in AI systems is increasingly mandatory.

MLOps in Fintech

Selecting the right model is only part of the equation. In fintech, models must operate reliably in production environments through strong MLOps practices. This includes deploying models into real time systems, monitoring for performance degradation, and retraining them as new data becomes available.

Fintech environments are particularly sensitive to model drift, where changes in user behavior or fraud patterns can reduce model accuracy over time.

Well-designed MLOps pipelines ensure continuous monitoring, automated retraining, and auditability. This transforms machine learning from a one-time implementation into a continuous, evolving system that remains accurate, compliant, and high performing.

10 Key Use Cases of Machine Learning in Fintech

Machine learning is now embedded across the financial lifecycle—from payments and lending to compliance and trading. The following use cases show how it actually works in production systems and the measurable impact it delivers.

1. Fraud Detection and Prevention

Fraud detection is the most advanced and widely deployed ML use case in fintech. These systems analyze transaction behavior, device fingerprints, geolocation, and network relationships to detect anomalies in milliseconds.

Unlike rule-based systems, ML models continuously learn from new fraud patterns, a principle that extends well beyond fintech, as explored in how ML is applied in cybersecurity, making them adaptive rather than reactive.

In practice, when a transaction occurs, the system builds a behavioral profile and compares it against historical patterns. If deviations are detected, such as unusual location or spending behavior, the model assigns a risk score and triggers an action instantly.

The results are significant. Visa reported that its AI systems prevented over $350 million in fraud attempts in 2024. Similarly, Danske Bank achieved a 60% reduction in false positives using ML-driven fraud detection. This directly improves customer experience by reducing unnecessary transaction blocks while increasing detection accuracy.

2. Credit Scoring and Alternative Data

Traditional credit scoring relies heavily on limited financial history. Machine learning expands this by incorporating alternative data sources such as transaction behavior, income patterns, and digital activity. This allows lenders to assess risk more accurately, especially for underserved populations.

In fintech systems, ML models analyze hundreds of features to predict default probability. These models are often combined with explainability tools like SHAP to ensure decisions remain transparent and compliant.

Companies like Upstart have demonstrated that ML-based underwriting can approve more borrowers without increasing risk.

3. Algorithmic and High Frequency Trading

Machine learning has become central to trading systems, where speed and prediction accuracy directly impact returns. Models such as LSTM networks analyze time-series market data, while NLP models process news, earnings reports, and sentiment signals.

These systems operate continuously, identifying patterns and executing trades faster than human traders. Reinforcement learning is also being used to optimize trading strategies dynamically based on market conditions.

4. Robo Advisors and Wealth Management

Robo-advisors use machine learning to automate investment decisions and deliver personalized financial advice. These systems analyze user goals, income, risk tolerance, and market conditions to create and manage portfolios.

Machine learning enables continuous portfolio optimization by adjusting asset allocations based on market movements and user behavior. This creates a dynamic investment strategy rather than a static one; platforms like Betterment and Wealthfront are leading examples.

The robo-advisory market is projected to grow significantly from approximately $14.08 billion in 2026 to $102.03 billion by 2034. If you are building in this space, the cost of building a banking or financial app is a practical starting point for scoping your investment."

5. RegTech, AML, and KYC Compliance

Regulatory compliance is one of the fastest-growing areas for machine learning in fintech. ML systems automate identity verification, transaction monitoring, and suspicious activity detection.

These systems analyze large volumes of transaction data to detect patterns associated with money laundering or fraud. Graph-based models and anomaly detection techniques help identify hidden relationships between accounts and transactions.

Banks are increasingly adopting ML for AML processes due to its efficiency and accuracy. For example, systems deployed by institutions like Danske Bank use AI to detect complex financial crime patterns that traditional systems miss. This reduces manual investigation workload while improving compliance outcomes.

6. Personalized Banking and Customer Experience

Machine learning enables banks to deliver highly personalized experiences by analyzing customer behavior, preferences, and transaction history. This allows institutions to recommend products, provide financial insights, and improve engagement.

NLP-powered chatbots and virtual assistants are a key component of this use case. These systems understand user intent, respond to queries, and even perform financial tasks.

For example, Bank of America’s AI assistant Erica serves over 42 million users and handles millions of interactions daily, demonstrating the scale of ML-driven customer engagement. Personalization not only improves user experience but also increases product adoption and retention.

7. Insurance Underwriting and Claims Processing

In insurance, machine learning improves both risk assessment and claims management. Models analyze data from telematics, wearables, and behavioral patterns to price policies more accurately.

For claims processing, ML systems automate document verification and fraud detection. They can quickly identify inconsistencies in claims data, reducing fraud and speeding up approvals.

This leads to faster claim settlements, lower operational costs, and improved customer satisfaction. InsurTech companies are leveraging ML to create dynamic pricing models and real-time risk evaluation systems.

8. Market Risk and Portfolio Management

Machine learning is increasingly used to assess financial risk and optimize portfolios. These models simulate market conditions, forecast liquidity, and calculate risk metrics such as Value at Risk.

Large institutions process massive datasets to feed these models. For instance, BNY Mellon processes trillions in transactions, which are used to train AI systems for risk analysis.

ML enables more accurate stress testing and scenario analysis, helping institutions make better investment decisions and manage risk more effectively.

9. Open Banking and Embedded Finance

Open banking initiatives are creating new opportunities for machine learning by enabling access to financial data across institutions. Regulations like PSD3 are accelerating this trend.

ML models analyze aggregated financial data to generate insights, recommend products, and power embedded finance experiences within non-financial platforms.

For example, fintech apps can use ML to offer personalized loans or insurance directly within their ecosystem. This creates uninterrupted financial experiences while increasing revenue opportunities.

10. Loan Automation and Digital Lending

Machine learning is transforming digital lending by automating underwriting and decision-making processes. Models evaluate borrower data instantly, reducing approval times from days to minutes.

These systems analyze multiple data points, including transaction history and behavioral signals, to assess risk more accurately than traditional methods.

Industry estimates show that over 60% of fintech lenders now use ML-driven credit scoring, enabling faster and more smooth lending operations. This improves efficiency while maintaining strong risk control.

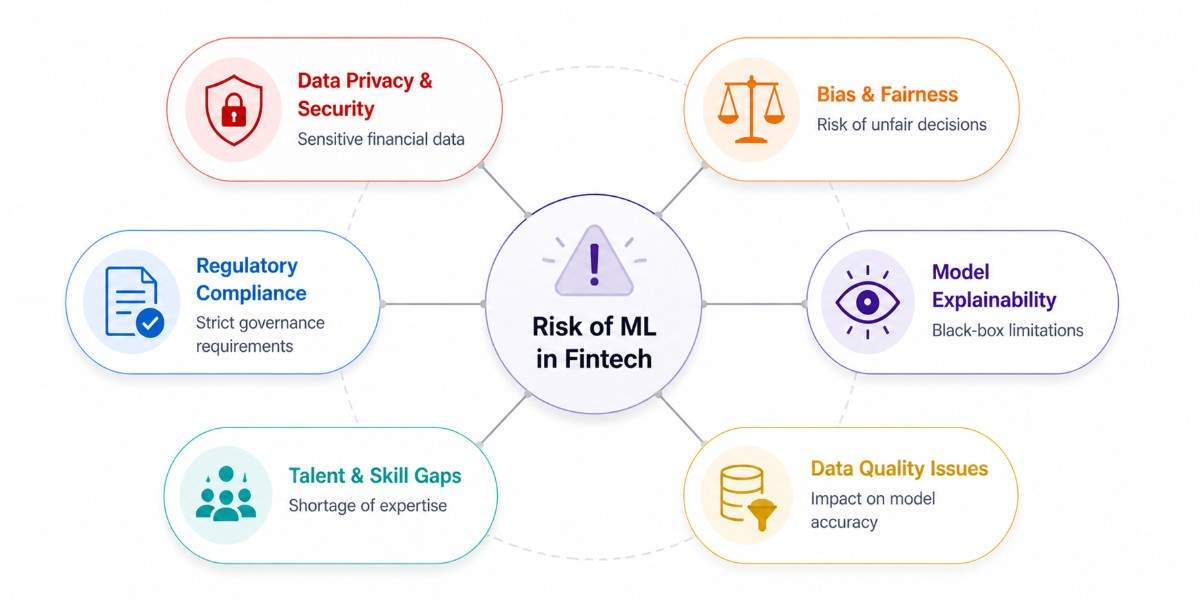

Challenges and Risks of Machine Learning in Fintech

Machine learning delivers strong advantages in fintech, but it also introduces risks that are technical, regulatory, and operational. In 2026, these challenges are no longer optional considerations; they directly impact compliance, system reliability, and business outcomes. The key is not just identifying the risks, but building systems that proactively address them.

Data Privacy and Security

Financial data is among the most sensitive categories of data, making privacy a critical concern. Machine learning models often require large datasets that include transaction histories, personal identifiers, and behavioral patterns. This creates risks around data leakage, misuse, and regulatory violations.

Modern fintech systems are adopting privacy-preserving machine learning techniques such as federated learning, where models are trained across distributed data without moving it to a central server. Techniques like differential privacy add controlled noise to datasets, ensuring individual data points cannot be reverse-engineered.

Compliance with frameworks influenced by the Reserve Bank of India and GDPR standards requires strong encryption, access controls, and audit mechanisms. Privacy must be designed into the ML pipeline from the start, not added later.

Bias and Fairness in Decision Making

Machine learning models can unintentionally inherit biases from historical data, leading to unfair outcomes in areas like credit scoring or lending. This is particularly risky in fintech, where decisions directly affect individuals’ financial access.

Bias mitigation starts with diverse and representative training datasets and continues through model evaluation. Techniques like SHAP analysis help identify how features influence decisions, making it easier to detect biased patterns.

Fairness-aware training methods can be applied to reduce discriminatory outcomes. Research highlighted by the Harvard Business Review shows that properly designed ML systems can improve fairness compared to traditional human-driven processes, but only when actively monitored and governed.

Regulatory Compliance and Governance

Regulation around AI in finance is tightening globally. Machine learning systems used in areas like credit scoring and fraud detection are increasingly classified as high-risk, requiring strict oversight and documentation.

Fintech companies must align with evolving frameworks such as the EU AI Act, which designates many financial ML systems as high-risk and mandates transparency, risk management, and human oversight. In the US, guidelines like SR 11-7 emphasize model risk management and validation.

Currently, only about 11 percent of European banks feel fully prepared for these requirements, and nearly 30 percent of AI budgets are now allocated to compliance, a pressure that is reshaping how teams hire and build AI/ML capability internally.

Building governance into ML systems, through model validation, documentation, and audit trails, is essential for long-term viability.

Model Explainability

Many advanced ML models, especially ensemble and deep learning models, operate as “black boxes.” In fintech, this lack of transparency is a major issue, particularly in regulated decisions like loan approvals or fraud flags.

Explainable AI (XAI) frameworks such as LIME and SHAP are increasingly used to interpret model outputs. These tools provide insights into why a decision was made, which is critical for both regulators and customers.

Financial institutions must also maintain clear audit trails, documenting how models are trained, validated, and deployed. Explainability is no longer optional; it is a regulatory expectation in many regions.

Talent Shortage and Skill Gaps

There is a significant shortage of professionals who understand both machine learning and financial systems. The demand for such hybrid expertise far exceeds supply, making hiring and retention a major challenge.

Organizations are addressing this gap by investing in cross-functional teams, combining data scientists with domain experts in finance and compliance. Many are also partnering with specialized development firms to accelerate implementation.

The market reflects this demand, with ML-fintech roles commanding 40 to 60 percent salary premiums and still facing a supply gap estimated at nearly four times demand. Strategic outsourcing and internal upskilling are becoming necessary to maintain momentum.

Data Quality and Feature Engineering

Machine learning models are only as good as the data they are trained on. In fintech, poor data quality, such as missing values, inconsistent records, or biased samples, can lead to inaccurate predictions and flawed decisions.

Strong data governance frameworks are essential. This includes standardized data pipelines, validation checks, and continuous monitoring of data quality.

Feature engineering plays a critical role in fintech, where raw transaction data must be transformed into meaningful signals. Organizations that invest in clean, well-structured data pipelines see significantly better model performance and reliability in production systems.

In 2026, the success of machine learning in fintech depends not just on model performance but on how well these risks are managed. The companies that lead are those that treat privacy, fairness, compliance, and data quality as core system requirements, not afterthoughts.

Future Trends in Machine Learning for Fintech

Machine learning in fintech is not a destination; it is a direction. The following trends are active in 2026 and will define the competitive landscape over the next three to five years.

Generative AI and LLMs Entering Financial Services

Large Language Models are moving from consumer novelty into production financial infrastructure. In 2026, LLMs power financial report generation, earnings summary extraction, contract analysis, regulatory document parsing, and sophisticated customer advisory chatbots that handle complex multi-turn financial conversations.

The distinction between 'traditional ML' and 'generative AI' is blurring; most production systems combine both, using ML for structured prediction tasks and LLMs for language understanding and generation.

Agentic AI - From Automation to Autonomous Action

The defining fintech technology shift of 2026 is agentic AI: systems that not only analyse and predict but take multi-step actions autonomously. An agentic fraud system does not just flag a suspicious transaction, it pauses it, generates a customer notification, initiates a verification flow, and updates the risk score, all without human intervention.

An agentic compliance agent monitors regulatory feeds, flags applicable changes, drafts policy updates, and routes them for human approval. This is agentic process automation (APA) replacing robotic process automation (RPA) as the efficiency driver of choice.

Federated Learning for Privacy-Preserving Collaboration

Federated learning allows multiple financial institutions to jointly train ML models, sharing the learning, not the data. A federated fraud model trained across 10 banks sees 10x the fraud patterns of any single institution's model, without any bank exposing its customer data to the others.

In 2026, several major banking consortia are actively running federated learning fraud and AML projects. This is the architecture that makes inter-institution ML collaboration legally possible under GDPR and CCPA.

Real-Time Payment Intelligence at Scale

The UK's Faster Payments and India's UPI processes billions more. At this scale, real-time fraud scoring is an ML problem of exceptional complexity; models must score every transaction within 500 milliseconds, 24 hours a day, with no batch processing window.

The ML infrastructure being built to support real-time payment networks is pushing the frontier of low-latency ML serving.

Asia Pacific as the Fastest-Growing ML Fintech Market

Asia-Pacific is forecast to grow at a 33.1% CAGR in AI fintech through 2031, the fastest of any region globally. China's heavy investment in generative AI, India's UPI-driven data ecosystem, and Southeast Asia's large unbanked population driving BNPL and alternative lending adoption are all fuelling this growth.

For companies operating in or building for the APAC market, ML investment is not optional; it is the price of market entry.

Explainable AI Becomes Regulatory Infrastructure

The EU AI Act has established a formal framework: ML systems that make or assist in consequential decisions about individuals; credit, insurance, and employment are high-risk systems requiring stringent oversight, documentation, and explainability.

Similar frameworks are developing in the US (FRB guidance) and UK (FCA model risk principles). By 2028, every regulated fintech operating in a major market will require a formal Model Risk Management function with XAI at its core.

Quantum ML on the Horizon

Quantum computing remains 3–7 years from widespread commercial deployment in finance, but IBM, JPMorgan, and Goldman Sachs are actively researching quantum-enhanced risk modelling, portfolio optimisation, and option pricing.

The theoretical advantage of quantum ML for certain financial problems, particularly Monte Carlo simulation and portfolio optimisation, is significant. Financial institutions with quantum research programmes are positioning early for when the technology matures.

Build Your ML-Powered Fintech Product with Code-B

Understanding machine learning in fintech is one thing. Building it reliably, at scale, in compliance with current regulations, is another. Code B specializes in developing ML-powered financial applications designed for real-world performance, scalability, and regulatory readiness.

We build production-grade ML systems across the fintech stack: fraud detection engines, alternative credit scoring platforms, KYC automation pipelines, robo-advisor backends, and algorithmic trading infrastructure. Our engagement model takes you from initial PoC through full MLOps deployment, with your team trained to own and iterate on the system after delivery.

Why Code-B:

- ISO-certified software development processes

- AWS Partner with cloud-native ML deployment capability

- Experience across fintech, neobanking, lending, and insurtech

- Clutch-rated with transparent delivery from India's tier-1 engineering talent pool

- US-based client engagement with offshore delivery economics

WhatsApp

WhatsApp Call Us

Call Us Mail Us

Mail Us