Everything you need to know about Banking API Integration

What Is Banking API Integration?

A Banking API is an interface that enables software systems to communicate with a bank's tech infrastructure.

Banking API integration refers to the process of connecting these APIs to your application or platform to enable data management and exchange.

In simple terms, a banking API enables one application to request services or data from a bank's system through structured endpoints.

Authorized applications can perform tasks such as retrieving account balances, initiating payments, or verifying customer identities without directly accessing core banking systems.

Why Integrate Banking APIs in Your Application?

Data Sharing and Instant Transactions

API integration allows systems to exchange financial data, retrieve balances, transaction histories, and payment confirmations instantly.

This ensures that users receive immediate feedback when performing financial actions such as transfers or payments.

For example, when a customer initiates a transaction through a mobile banking app, the request is processed through APIs that communicate with backend systems and return confirmation within seconds.

Embedded Financial Services

APIs allow businesses to integrate financial services directly into non-banking platforms, supporting new digital business models.

To execute this functionality, you'd have to use an extensible API ecosystem and modular service design.

E-commerce platforms, ride-sharing app services, and marketplaces can offer payments, lending, or payouts without building a full banking infrastructure.

Better Customer Experience in Digital Banking

Banking tech users expect fast, responsive, and intuitive financial applications. APIs support this by enabling data access, instant notifications, and seamless transaction processing.

Applications can dynamically retrieve and display relevant information, improving usability and reducing friction in financial interactions.

Fintech Partnerships

Banks collaborate with fintech companies by integrating APIs to expand their service offerings. These partnerships allow fintech platforms to build specialized solutions such as expense management tools, credit scoring systems, and investment applications.

At the same time, banks maintain control over data access and regulatory compliance, creating a balance between innovation and governance.

Operational Efficiency

API integration reduces reliance on manual processes by automating workflows such as payment processing, compliance checks, and customer verification.

This improves processing speed, lowers operational costs, and allows financial institutions to scale services more efficiently.

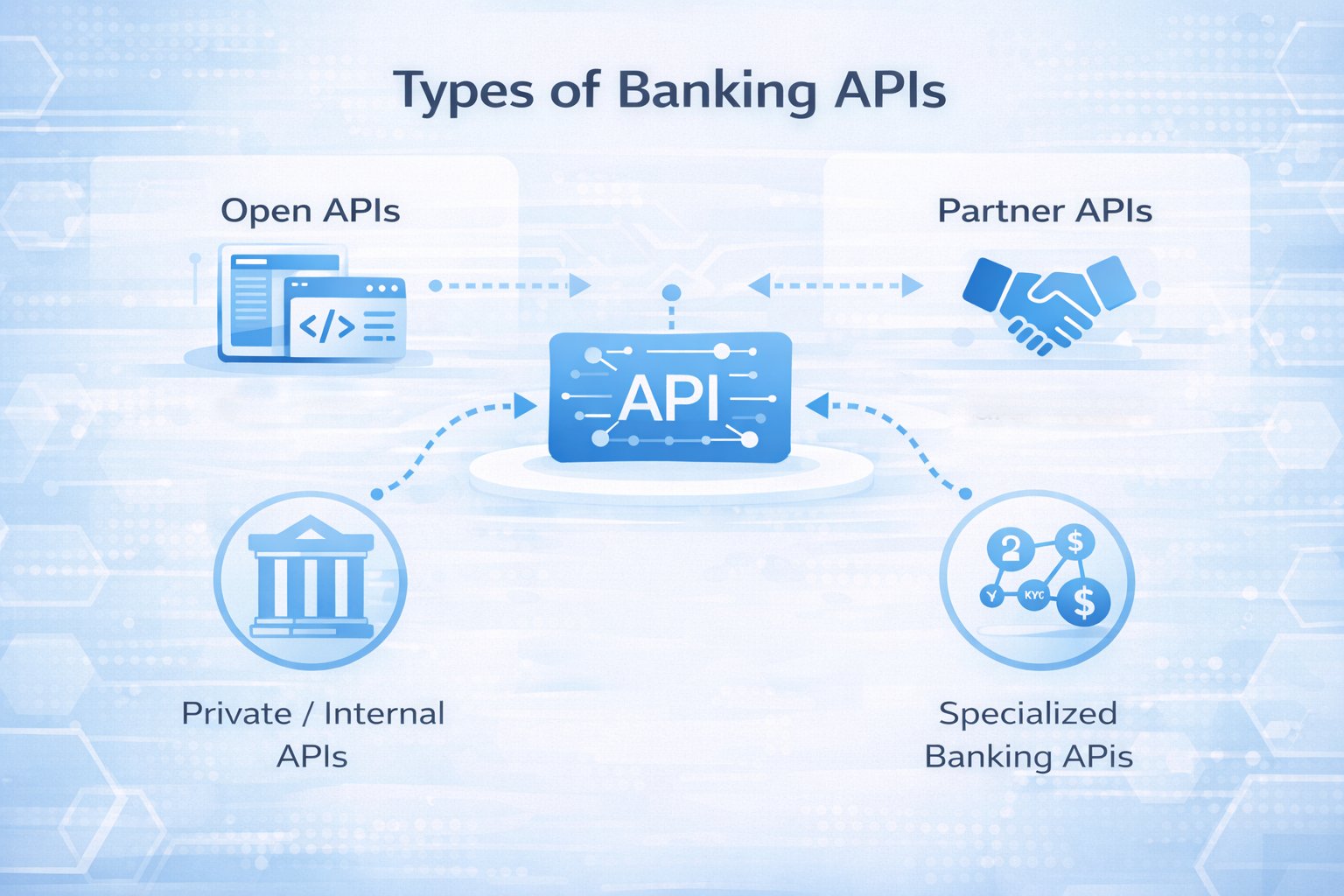

What Are the Different Types of Banking APIs?

Banking APIs come in several categories based on who can access them and how they are intended to be used.

These categories reflect different access levels and usage patterns that banks and fintech companies adopt to manage data sharing and service integration.

They can help you manage broad developer ecosystems, from tightly controlled partner integrations to internal system connectivity, while also supporting specialized APIs designed for specific financial workflows.

Open APIs

Open APIs are public interfaces that let outside developers and fintech platforms build apps on top of banking infrastructure.

Developer portals and sandbox environments are usually used to access these APIs. This makes it easier for third parties (outsourced dev team) to test, combine, and grow financial features.

The use of these APIs can help banks expand digital ecosystems by allowing them to extend their services beyond their own platforms.

Partner APIs

Partner APIs are designed for selected organizations that have established formal relationships with a bank.

These integrations allow collaborating partners to embed banking capabilities directly into their products or workflows.

Compared to open APIs, they offer more tailored functionality and are governed by stricter contractual and operational agreements.

Private / Internal APIs

Private or internal APIs operate within a bank’s internal systems to connect different services and applications.

They are essential for modernizing legacy infrastructure, enabling internal teams to build scalable architectures and streamline operations.

These APIs focus on maintaining system stability while supporting ongoing technological upgrades.

Specialized Banking APIs

Specialized APIs are built to handle specific financial processes such as onboarding, identity verification, payments, and lending workflows.

They encapsulate complex business logic into reusable services, allowing applications to execute targeted functions efficiently without needing to manage underlying complexities.

This combination of public, partner, internal, and specialized APIs forms a structured ecosystem that supports both innovation and control.

It allows banks to expand their capabilities while maintaining oversight of critical systems and data flows.

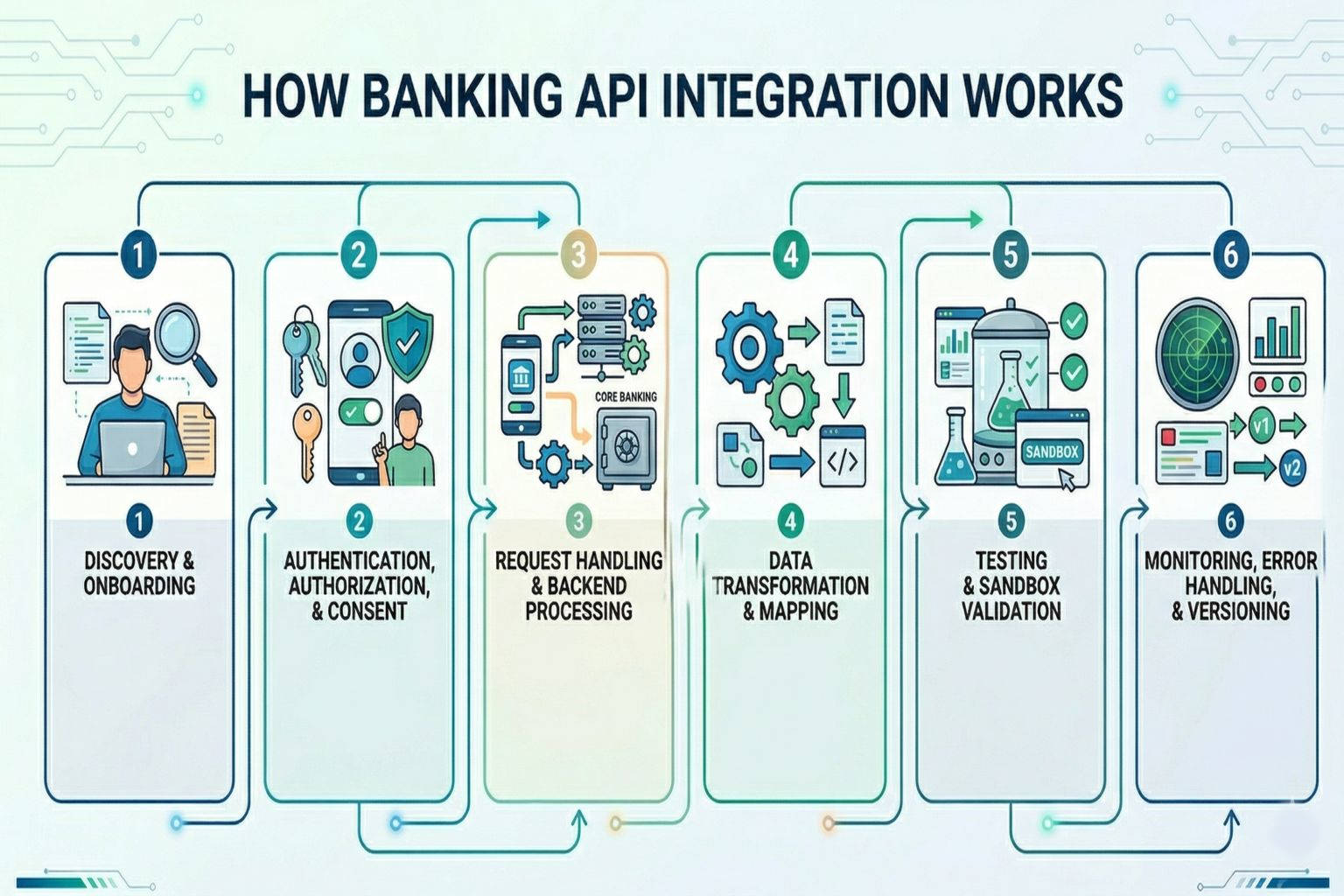

How Does a Banking API Work in Applications?

At a high level, API integration begins with discovery and authorization, moves through secure request and response exchanges, and concludes with monitoring and lifecycle management to ensure reliability and compliance.

Discovery and Onboarding

Developers begin by identifying available API endpoints and onboarding requirements through developer portals or partner documentation.

This process includes obtaining credentials, accessing sandbox environments, and agreeing to usage terms that define permitted data access and operational limits.

Authentication, Authorization, and Consent

Secure access is established through authentication and authorization mechanisms such as OAuth 2.0 or mutual TLS.

These ensure that only verified applications can interact with banking systems and that users explicitly grant permission for data sharing within defined scopes.

Request Handling and Backend Processing

When an application sends a request, it is routed through an API endpoint where validation and processing occur.

The request is then handled by backend systems such as core banking platforms, payment engines, or identity services, which generate a response returned to the application.

Data Transformation and Mapping

Integration often requires transforming data between different formats and structures. Mapping layers ensure compatibility between external API payloads and internal banking systems while enforcing validation rules and data policies.

Testing and Sandbox Validation

Before deployment, integrations are tested in sandbox environments that replicate real API behavior without exposing live customer data.

This allows developers to validate workflows, handle edge cases, and ensure stability.

Monitoring, Error Handling, and Versioning

Once deployed, integrations require continuous monitoring to track performance, detect failures, and maintain reliability.

Error handling mechanisms and versioning strategies help ensure that updates can be introduced without disrupting existing services.

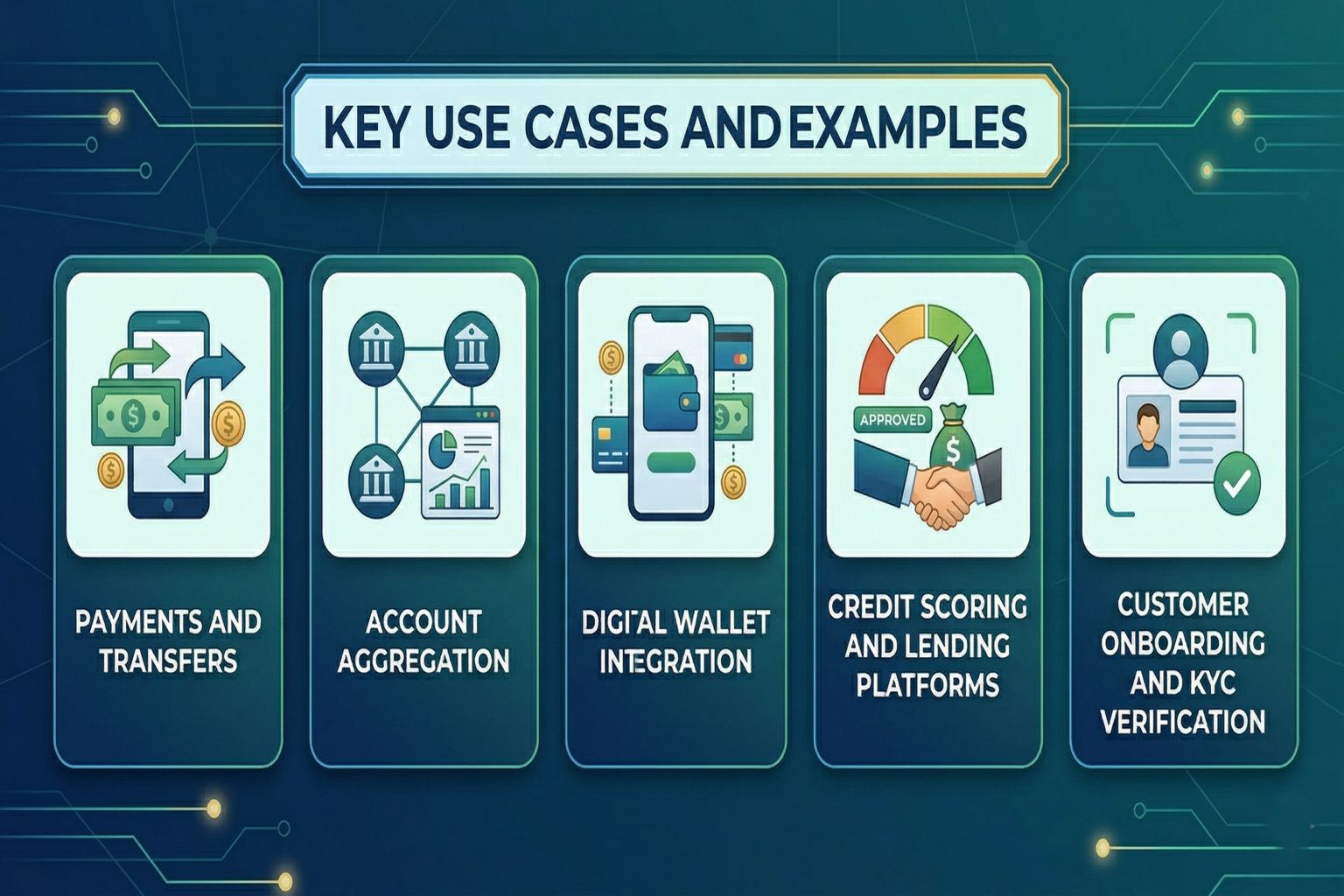

Common Use Cases of Banking APIs

Banking API integration powers a wide range of financial applications by enabling secure and automated workflows across platforms.

Payments and Transfers

Payment APIs allow applications to initiate and process transactions directly from user accounts. Platforms like food delivery or e-commerce apps utilise these APIs to provide seamless payment experiences without redirecting users to external systems.

Account Aggregation

APIs allow aggregation services to collect financial data from multiple institutions and present it within a single interface. Users are able to access a consolidated view of their financial position, improving visibility and financial planning.

Digital Wallet Integration

Digital wallets rely on APIs to connect with bank accounts, retrieve account details, and process transactions. This integration supports features such as balance checks, payments, and transaction history within wallet applications.

Credit Scoring and Lending Platforms

Lending platforms use APIs to access financial data required for evaluating loan applications. This allows faster credit assessment by analyzing transaction history, income patterns, and existing obligations.

Customer Onboarding and KYC Verification

APIs support digital onboarding processes by enabling identity verification, compliance checks, and document validation. As a result, financial institutions can access fully digital account creation with reduced manual intervention.

How to Ensure Security and Compliance in Banking APIs

When integrating banking APIs, executing reliable security practices is very important because financial data must be kept safe from unauthorized access while still meeting strict legal requirements.

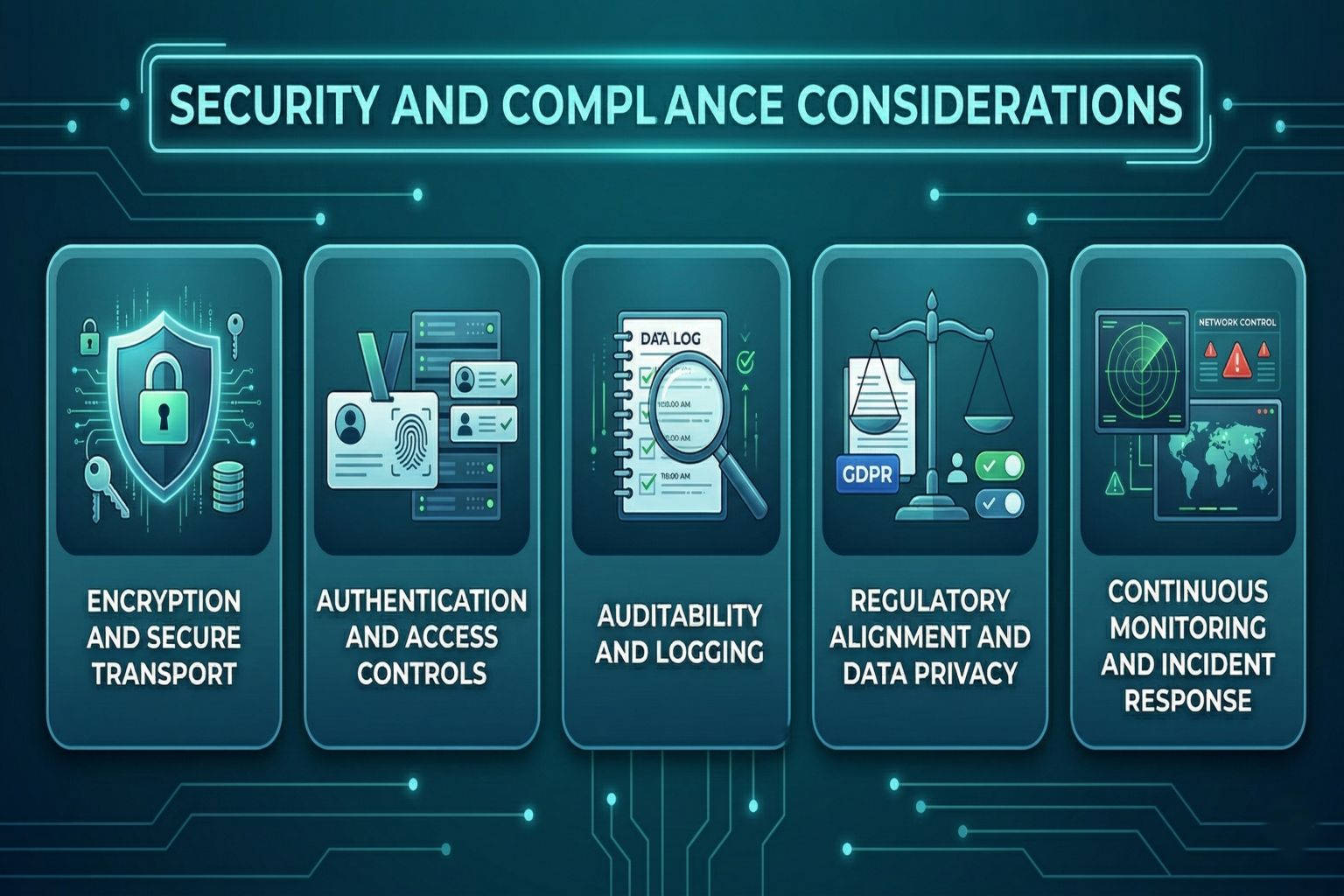

Encryption and Secure Transport

Encryption protocols like TLS are used to secure all data exchanged through banking APIs, guaranteeing confidentiality and integrity throughout transmission. Tokenization can also be used to lessen sensitive data exposure.

Authentication and Access Controls

Access controls guarantee that only authorized data and services are accessible, while authentication mechanisms confirm the identities of users and applications. These safeguards aid in preventing abuse and unapproved system interactions.

Auditability and Logging

Detailed logging and audit trails are maintained to track data access and system activity. These records are critical for regulatory compliance, security investigations, and operational transparency.

Regulatory Alignment and Data Privacy

The regulatory frameworks and data privacy laws that control the sharing and processing of financial data must be adhered to by banking API integrations. This covers cross-border data handling, data minimization, and user consent management.

Continuous Monitoring and Incident Response

Organizations use ongoing surveillance to find anomalous activity and possible dangers. Mechanisms for responding to incidents guarantee that security breaches are promptly detected, contained, and fixed to reduce their impact.

What Makes Banking API Integration Challenging?

There are a few operational and technical difficulties when implementing API integration for bank technology, despite the usefulness of API connectivity.

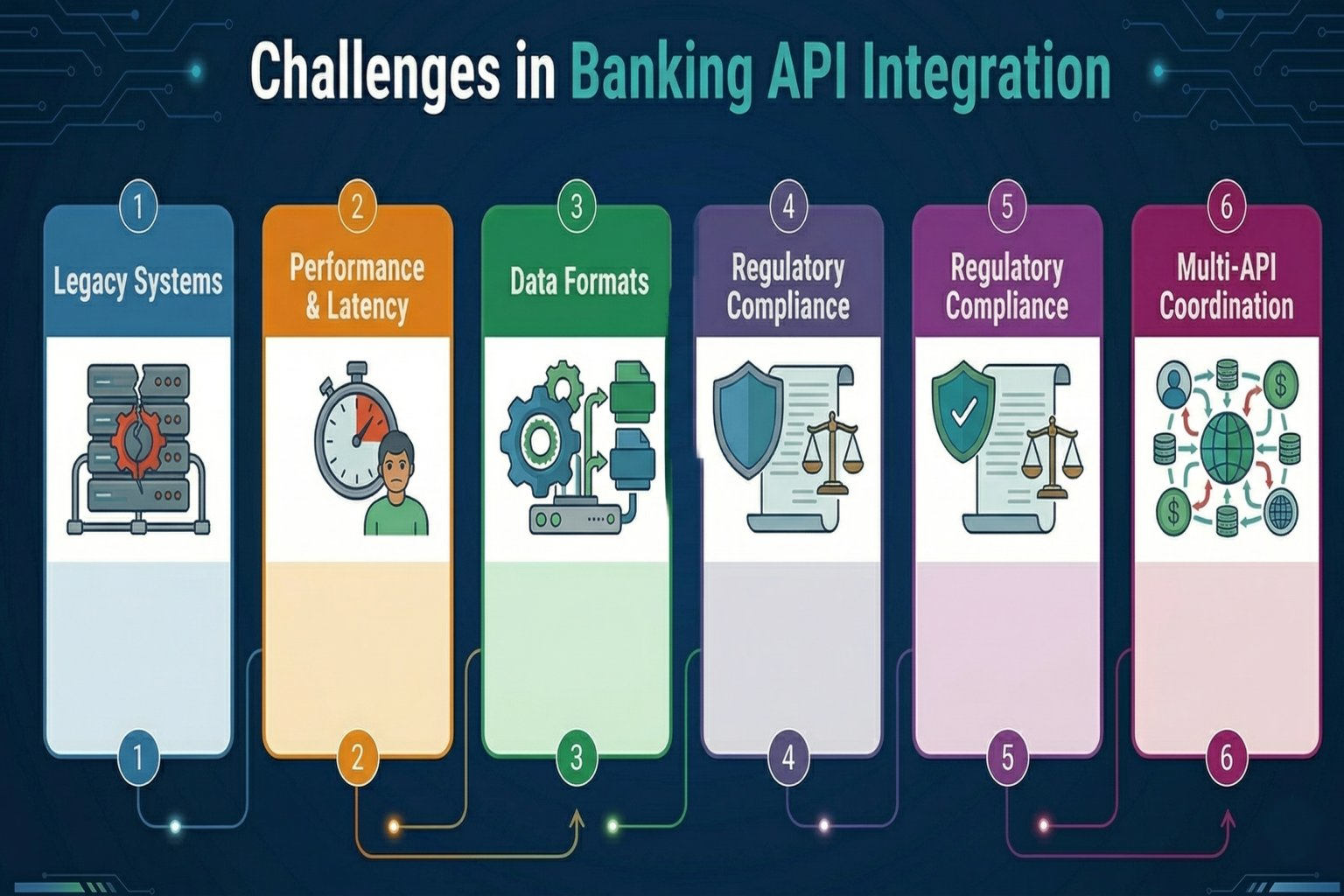

Legacy Banking Systems

Many banks operate on legacy infrastructure that is not optimized for modern API integration. Updating or integrating these systems often requires additional layers such as middleware, which can increase complexity and development effort.

Performance and Latency Management

Financial applications require fast response times to maintain user trust and system reliability. Delays in API responses can lead to failed transactions, poor user experience, and operational inefficiencies.

Data Format Differences

Different systems may use varying data formats such as JSON or XML. Integration requires mapping and transformation layers to ensure consistent communication between systems.

Regulatory Compliance

Compliance with financial regulations adds complexity to API integration. Systems must be designed to meet strict security, reporting, and data handling requirements.

Multi-API Coordination

Modern applications often depend on multiple APIs working together. Coordinating these integrations requires careful orchestration to ensure consistency, reliability, and seamless user experiences.

Best Practices for Successful Banking API Integration

Organizations that integrate banking APIs successfully follow practices that ensure reliability, security, and scalability.

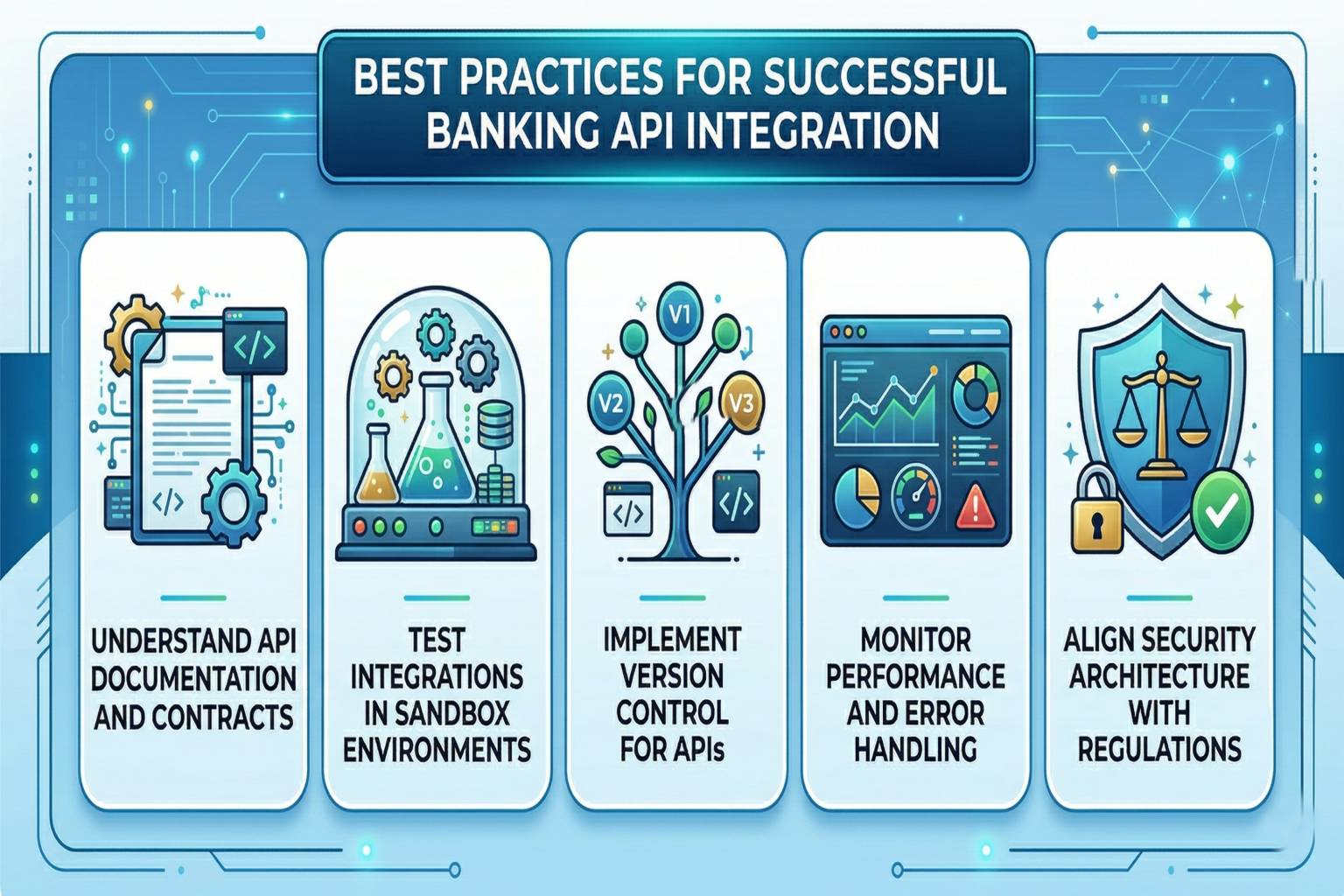

Understand API Documentation and Contracts

A thorough understanding of API documentation helps developers correctly implement endpoints, authentication methods, and data structures. It ensures that integrations follow expected request and response formats, reducing the likelihood of errors.

Clear knowledge of API contracts also improves coordination between systems and teams. This foundation helps avoid misconfigurations that can lead to failures during execution.

Test Integrations in Sandbox Environments

Testing in sandbox environments allows teams to validate workflows in a controlled setting without impacting real users or financial data. It helps identify edge cases, unexpected responses, and performance issues before moving to production.

Early validation reduces deployment risks and improves overall system stability. Sandbox testing also enables safe experimentation with different scenarios and configurations.

Implement Version Control for APIs

API versioning allows systems to evolve without disrupting existing integrations that depend on earlier versions. It supports the gradual adoption of new features while maintaining backward compatibility for ongoing operations.

This approach ensures stability across applications that rely on consistent API behavior. Proper version control also simplifies maintenance and long-term system scalability.

Monitor Performance and Error Handling

Continuous monitoring helps track API performance metrics such as response times, availability, and failure rates. Identifying issues early allows teams to address bottlenecks before they impact users.

Effective error handling ensures that applications can respond appropriately to failures, maintaining a consistent user experience. Together, these practices improve reliability and operational efficiency.

Align Security Architecture with Regulations

Security measures must align with regulatory requirements to ensure compliance and protect sensitive financial data. This includes implementing strong authentication, encryption, and access controls across all API interactions.

Regulatory alignment also requires maintaining audit trails and monitoring for suspicious activity. A well-defined security approach ensures both data protection and long-term system trustworthiness.

Future Trends in Banking API Integration

Banking API ecosystems are evolving rapidly as new technologies and business models expand their role in digital finance.

AI-Enhanced API Services

APIs are increasingly incorporating AI capabilities to support functions such as fraud detection, credit risk evaluation, and personalized financial insights.

These integrations enable systems to analyze large volumes of financial data in real time and generate actionable outcomes. AI-driven APIs can improve decision-making accuracy and automate complex processes. As adoption grows, they will play a key role in enhancing efficiency and user experience.

Real-Time and Event-Driven APIs

Event-driven architectures are enabling APIs to deliver real-time updates instead of relying on periodic requests. This shift supports instant transactions, live balance updates, and immediate notifications for financial activities.

It improves system responsiveness and aligns with user expectations for real-time interactions. As financial services continue to evolve, real-time capabilities will become a standard requirement.

Embedded Finance and API Marketplaces

Financial services are increasingly being embedded into non-financial platforms through API-driven models. This allows businesses to offer payments, lending, or insurance directly within their applications.

API marketplaces further simplify integration by providing standardized access to multiple financial services in one place. This trend is driving the expansion of financial capabilities across diverse digital platforms.

Interoperability and Standardization

Efforts toward standardizing API formats and consent frameworks are improving compatibility between different financial systems. Standardization reduces integration complexity and enables smoother data exchange across platforms and regions.

It also supports regulatory alignment by ensuring consistent data-sharing practices. As standards evolve, they will make large-scale integrations more efficient and scalable.

Blockchain and Decentralized Integrations

Blockchain technologies are being explored to support new financial infrastructure models, including programmable transactions and decentralized identity systems. APIs can act as bridges between traditional banking systems and decentralized networks, enabling hybrid integrations.

These developments may introduce new ways of handling transactions, verification, and data ownership. As the technology matures, it could reshape parts of the financial ecosystem.

Summing Up

The concept of integrating APIs with banking tech infrastructure has laid the foundation for a reliable connection between banks and financial platforms and digital applications.

It allows financial services to move beyond traditional boundaries and integrate directly into everyday digital experiences.

Organizations that implement API integrations effectively can build more flexible systems, respond faster to market demands, and deliver more connected user experiences.

At the same time, success depends on maintaining a balance between openness and control. Strong security practices, regulatory compliance, and thoughtful system design are essential to ensuring that integrations remain reliable and secure as they scale.

WhatsApp

WhatsApp Call Us

Call Us Mail Us

Mail Us